Professional Liability

“If you offer service(s) to others, you need E&O” – Oscar Paz

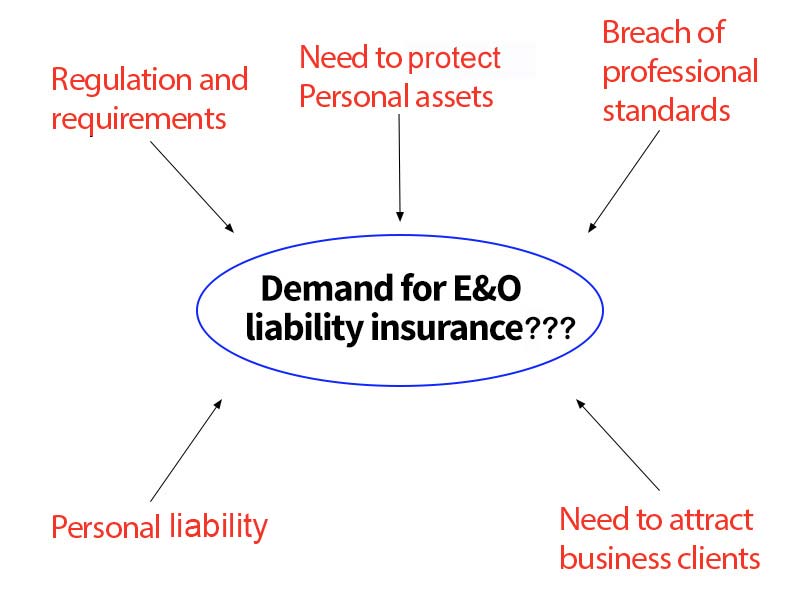

Professional liability more commonly known as errors & omissions (E&O) is a form of liability insurance that helps protect professional advice- and service-providing individuals and companies from bearing the full cost of defending against a negligence claim made by a client, and damages awarded in such a civil lawsuit. The coverage focuses on alleged failure to perform on the part of, financial loss caused by, and error or omission in the service or product sold by the policyholder. These are causes for legal action that would not be covered by a more general liability insurance policy which addresses more direct forms of harm. Professional liability coverage sometimes also provides for the defense costs, including when legal action turns out to be groundless. Professional liability insurance is required by law in some areas for certain kinds of professional practice (especially medical and legal), and is also sometimes required under contract by other businesses that are the beneficiaries of the advice or service.

Professional liability insurance may take on different forms and names depending on the profession. For example, in reference to medical professions it is called malpractice insurance, while errors and omissions (E&O) insurance is used by insurance agents, consultants, brokers and lawyers. Other professions that commonly purchase professional liability insurance include accounting, engineering and financial services, construction and maintenance (general contractors, plumbers, etc., many of whom are also surety bonded), and transport. Some charities and other nonprofits/NGOs are also professional-liability insured.

The primary reason for professional liability coverage is that a typical general liability insurance policy will only respond to a bodily injury, property damage, personal injury or advertising injury claim. Other forms of insurance cover employers, public and product liability. But various professional services and products can give rise to legal claims without causing any of the specific types of harm covered by such policies. Common claims that professional liability insurance covers are negligence, misrepresentation, violation of good faith and fair dealing, and inaccurate advice. Examples.

- If a software product fails to perform properly, it may not cause physical, personal, or advertising damages, therefore the general liability policy would not be triggered; it may, however, directly cause financial losses which could potentially be attributed to the software developer's misrepresentation of the product capabilities.

- If a custom-designed product fails without causing damage to person or property other than to the subject product itself, a product liability policy may cover consequential damages such as losses from business interruption, but will generally not cover the cost to redesign, repair or replace the failed product itself. Claims for these losses against the manufacturer may be covered by a professional liability policy.

- Professional liability insurance policies are generally set up based on a claims-made basis, meaning that the policy only covers claims made during the policy period. More specifically a typical policy will provide indemnity to the insured against loss arising from any claim or claims made during the policy period by reason of any covered error, omission or negligent act committed in the conduct of the insured's professional business during the policy period. Claims which may relate to incidents occurring before the coverage was active may not be covered, although some policies may have a retroactive date, such that claims made during the policy period but which relate to an incident after the retroactive date (where the retroactive date is earlier than the inception date of the policy) are covered.

As you may know, business liability insurance covers losses related to bodily injury, property damage or advertising injury. But what happens, and who pays, when a printer neglects to catch a typographic error on a large order of engraved wedding invitations? Or when a plumbing repair fails and causes an entire office to be flooded?

Issues like these can be resolved with the purchase of errors and omissions (E&O) insurance. Errors and omissions insurance is a kind of specialized liability protection against losses not covered by traditional liability insurance. It protects you and your business from claims if a client sues for negligent acts, errors or omissions committed during business activities that result in a financial loss for the client.

Costly mistakes can happen – even to people with the best training and years of experience. It’s human nature. That’s why errors and omissions insurance is so important.

Errors and omissions insurance policies vary from company to company, and are written to reflect inherent risks and common exposures particular to different types of businesses.

Some events resulting in a loss for a client may have occurred several years in the past, and the first time the mistake is apparent is when a court summons arrives in the mail. That’s when the retroactive date on the policy is very important. The farther back the retroactive date of the policy, the more coverage and protection it offers.

“Please see polic(ies) and endorsement(s) for exact terms, conditions and exclusions. Each insurance company has its own policy language. We encourage you to seek legal advice prior to securing any insurance."

Marketing

Application

- Consultant Services

- Media/Advertising Services

- Employment/Staffing Organizations

- Miscellaneous Services

- Financial Services

- Insurance Related Services

- Real Estate/Environment

- Technology

- Legal Services

- Travel

Claims Examples

Articles

- Call to Duty

by Peter R. Taffae, Risk & Insurance - Insureds Need To Sort Out Potential Hammer Effects

by Peter R. Taffae, National Underwriter Property & Casualty - Lawyers Should Not Dismiss Lawyers' Professional Liability Coverage

by Damien Magnuson, Insurance Journal

Other